What tax incentives exist to help families pay for college?

Rapidly rising college expenses in the 1990s spurred the 1997 enactment of tax incentives for higher education, which currently include the American opportunity tax credit, the lifetime learning credit, and the student loan interest deduction.

American Opportunity Tax Credit

The American opportunity tax credit (AOTC) provides a credit up to $2,500 per student during the first four years of undergraduate postsecondary school. Students receive a credit of 100 percent against the first $2,000 of tuition, fees, and books, and a 25 percent credit against the next $2,000. Up to $1,000 of the AOTC is refundable; to qualify for the credit, students must be enrolled at least half time for one or more academic periods during the year. AOTC credits, it should be noted, are not indexed for inflation. The AOTC was enacted as part of the 2009 (?) fiscal stimulus package and then made permanent in 2015 under the Protecting Americans from Tax Hikes Act. The AOTC replaced the Hope credit enacted in 1997 and is available for more years of schooling (four versus two years), covers more expenses, and is partly refundable.

The maximum benefit for the AOTC begins to phase out when modified adjusted gross income (MAGI) reaches $80,000 and is completely phased out at MAGI of $90,000. For married couples, the phaseout range begins at MAGI of $160,000 and the credit is completely phased out at MAGI of $180,000. The phaseout thresholds are not indexed for inflation.

Lifetime Learning Credit

The lifetime learning credit (LLC) equals 20 percent of tuition and fees for any postsecondary education expense, up to a maximum annual credit of $2,000 per taxpayer. That maximum applies to the combined expenses of all students in the household claiming the credit and is reached when total qualifying expenses equal $10,000. Like the AOTC, the maximum benefit for the LLC phases out for MAGI between $80,000 and $90,000 (and between $160,000 and $180,000 for married couples). The phaseout thresholds for the lifetime learning credit are adjusted annually for inflation. The LLC is nonrefundable, so only people who owe income tax can benefit.

Student Loan Interest Deduction

The student loan interest deduction allows taxpayers with qualified student loans (loans taken out solely to pay qualified higher education expenses) to reduce taxable income by $2,500 or the interest paid during the year, whichever is less. The loan cannot be from a relative or made under a qualified employer plan, and the student must be a taxpayer, a spouse, or a dependent; only those enrolled at least half time in a degree program qualify.

Qualified expenses include tuition and fees; room and board; books, supplies and equipment; and other necessary expenses such as transportation. To qualify in 2022, a taxpayer’s AGI may not exceed $85,000 for single, head of household, or qualifying widower filers, or $175,000 for married filers. After that, a family is no longer eligible for the deduction. The deduction is available to taxpayers who do not itemize deductions but is, of course, only valuable to people with taxable income. The student loan interest deduction is projected to cost an estimated $2.4 billion in 2024.

How These Tax Incentives Affect Students

Before Congress created the AOTC, many observers argued that existing tax subsidies had minimal impact on college enrollment because those subsidies went mostly to people who would have attended college even without the additional aid. Many low-income students who might have been the most influenced by reduced college costs received little or no benefit from the Hope credit and the LLC because they were nonrefundable and thus could only offset income taxes owed.

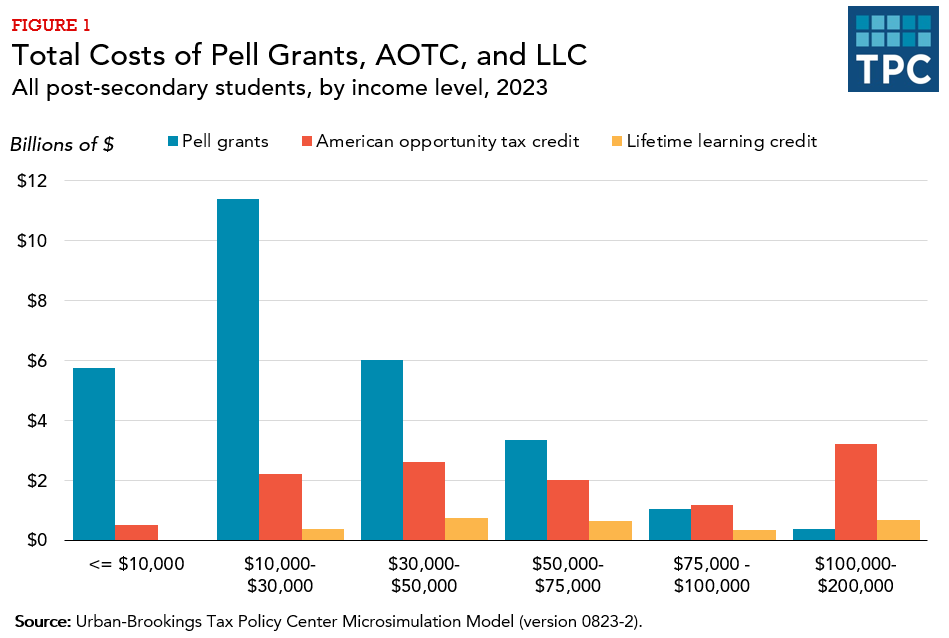

In response, the AOTC was made refundable, allowing lower-income families to receive the credit. Even so, students with incomes below $75,000 receive more aid from the Pell grant than from the tax credits (figure 1). Even with recent changes to tax credits, it remains unclear whether tax credits increase college enrollment.

Using the tax system to subsidize higher education has two primary advantages over using traditional spending programs: (1) students don’t have to fill out the daunting Free Application for Federal Student Aid form to receive benefits, and (2) every student who qualifies receives the full benefit for which he or she appears entitled. However, providing aid through the tax system also has disadvantages—notably, the delay in funds being received (up to 15 months after tuition was paid), a lack of transparency about why taxes went down, and potential mismatches in that the person receiving the credit or deduction is often not the student.

Options for Reform

Even though some books are eligible expenses under the American opportunity tax credit, additional assistance could be provided by broadening coverage to include a fixed amount of living expenses for all students.

Providing benefits directly to schools when students enroll—not months later when their families file tax returns—could help students cover college costs when they are obliged to make payments. Benefit amounts would be based on estimates of the previous year’s taxes.

Consolidating the credits into a single credit would make the process more transparent for students and taxpayers.

Rather than offering a deduction for student loan interest, providing incentives for students to enroll in income-contingent repayment programs would reduce hardship in student debt repayment.

Updated January 2024

Joint Committee on Taxation. 2022. “Estimates of Federal Tax Expenditures for Fiscal Years 2022–2026.” JCX-22-22. Washington, DC

Baum, Sandy, and Martha Johnson. 2015. “Student Debt: Who Borrows Most? What Lies Ahead?.” Washington, DC: Urban Institute.

Bulman, George B., and Caroline M. Hoxby. 2015. “The Returns to the Federal Tax Credits for Higher Education.” NBER Working Paper No. 20833. Cambridge, MA: National Bureau of Economic Research.

Crandall-Hollick, Margot. 2021. “Higher Education Tax Benefits: Brief Overview and Budgetary Effects.” Washington, DC: Congressional Research Service.

Dynarski, Susan, and Judith E. Scott-Clayton. 2007. “College Grants on a Postcard: A Proposal for Simple and Predictable Federal Student Aid.” Hamilton Project Discussion Paper. Washington, DC: Brookings Institution.

Dynarski, Susan, Judith Scott-Clayton, and Mark Wiederspan. 2013. “Simplifying Tax Incentives and Aid for College: Progress and Prospects.” NBER Working Paper No. 18707. Cambridge, MA: National Bureau of Economic Research.

Internal Revenue Service. 2022. “Tax Benefits for Education (For Use in Preparing 2022 Returns).” Publication 970. Washington, DC.

New America Atlas. 2015. “Higher Ed Tax Benefits.”

Rueben, Kim, and Sandy Baum. 2015. “Obama Would Improve Tax Subsidies for Higher Education.” Tax Vox (blog). Washington, DC: Urban-Brookings Tax Policy Center.