Possible reforms run the gamut from repeal to modest fixes that would make the estate tax more difficult to avoid.

Proposals to reform the estate and gift tax range from comprehensive options, such as permanently repealing the estate tax or replacing the existing tax with a tax on inheritances, to more modest options, such as decreasing exemption amounts, increasing tax rates, and blocking avenues for avoidance.

The federal estate and gift taxes (including the generation-skipping tax, or GST) have changed more than a dozen times since 2001. The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) cut these taxes sharply but only through 2010. EGTRRA gradually phased out the estate tax and GST, eliminating them entirely for 2010 and leaving only the gift tax (at a reduced rate) in that year. It also would have limited carryover basis for assets transferred in that year.

The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 reinstated the estate tax and GST for 2010 and extended them through 2012, with a $5 million estate tax exemption (indexed for inflation after 2011) and a top rate of 35 percent. But the law allowed executors to elect the EGTRRA rules for decedents who died in 2010. The American Taxpayer Relief Act of 2012 (ATRA) permanently extended the 2012 rules, though with a new top rate of 40 percent.

The Tax Cuts and Jobs Act of 2017 (TCJA) doubled the estate tax exemption to $11.18 million in 2018 (indexed for inflation after 2018) but kept the 40 percent top rate. The TCJA changes expire after 2025.

Repeal

Many members of Congress have called for the repeal of the estate and gift taxes. That would be expensive, however. The Office of Management and Budget projects that these taxes will raise $466 billion in fiscal years 2024 through 2033.

Repeal would also be regressive—the benefits would go almost entirely to people at the top of the income distribution—and would invite significant sheltering of income. Further, gifts from an estate to charity currently qualify for full deduction from the taxable estate, creating a substantial incentive to leave bequests to charities. Prior estimates indicate that repealing the estate tax would reduce charitable donations by 6 to 12 percent.

Inheritance Tax

One option, the substitution of an inheritance tax, would tax wealth transfers differently. An inheritance tax differs from an estate and gift tax in that the rate depends on the amount of gifts and bequests the taxpayer receives rather than on how much the donor gives or bequeaths.

Unlike estate and gift taxes, a progressive inheritance tax gives donors an incentive to spread their wealth more broadly, because each of any number of recipients can claim an exemption and take advantage of progressive tax rates, thus reducing the total tax attributable to an estate. Most countries that tax wealth transfers do so with inheritance taxes rather than estate taxes and many states levy inheritance taxes.

Limit Preferences

A more modest reform could repeal or modify the many estate tax preference items, such as special trust arrangements and valuation discounts, that allow savvy millionaires to drastically reduce or even eliminate estate tax liability. University of Southern California law professor Edward McCaffery said the tax was so easy to avoid that it was essentially a “voluntary tax” (albeit one that raised about $20 billion per year at the time of his writing). The plethora of loopholes complicates estate planning and results in comparable estates facing very different tax bills. Eliminating estate tax preferences could increase revenues, which could pay for extending the higher estate tax exemption scheduled to return to pre-TCJA levels after 2025 or for reducing the deficit.

Return to Prior Law

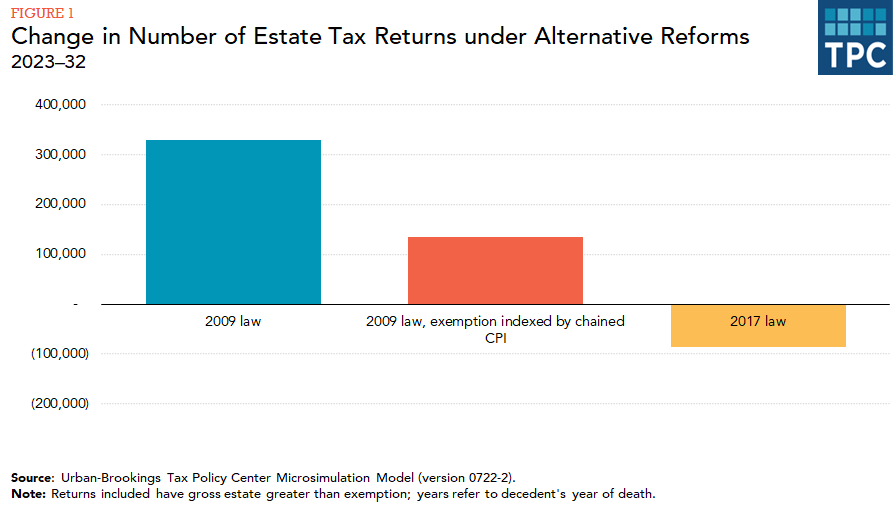

Alternatively, policymakers might simply reverse some of the estate tax changes enacted since 2001 (figure 1).

2009 law: The estate tax law in effect under EGTRRA for 2009 had an exemption of $3.5 million (unindexed) and a top rate of 45 percent. If 2009 law were made permanent starting in 2023, the number of estate tax returns filed for decedents who died between 2023 and 2032 would increase by 329,000, and estate tax liabilities of these decedents would increase by $364 billion.

2009 law, exemption indexed by chained consumer price index: If 2009 law, modified to index the exemption to inflation, were made permanent starting in 2023, the number of estate tax returns filed for decedents who died between 2023 and 2032 would increase by 135,000, and estate tax liabilities of these decedents would increase by $218 billion (about six-tenths the increase without indexing the exemption).

2017 law: The TCJA doubled the estate tax exemption and adopted a somewhat slower inflation adjustment starting in 2018, but only through 2025. Making the TCJA permanent by maintaining the $10 million exemption (indexed for inflation from 2011) after 2025 would decrease the number of estate tax returns filed by 85,000 between 2025 and 2032 and would reduce estate tax liabilities by about $131 billion.

Updated January 2024

Bakija, Jon M., and William G. Gale. 2003. “Effects of Estate Tax Reform on Charitable Giving.” Washington, DC: Urban-Brookings Tax Policy Center.

Batchelder, Lily L. 2009. “What Should Society Expect from Heirs? A Proposal for a Comprehensive Inheritance Tax.” Tax Law Review 63 (1): 1–112.

Batcheler, Lily 2020. “Leveling the Playing Field Between Inherited Income and Income From Work Through an Inheritance Tax.” In Emily Moss, Ryan Nunn, and Jay Shambaugh, editors. Tackling the Tax Code: Efficient and Equitable Ways to Raise Revenue. Washington, DC: Brookings Institution.

Joint Committee on Taxation. 2015. “History, Present Law, and Analysis of the Federal Wealth Transfer System.” JCX-52-15. Washington, DC.

Joint Committee on Taxation. 2018. “Overview of the Federal Tax System as in Effect for 2018.” JCX-3-18. Washington, DC.

McCaffery, Edward J. 2000. “A Voluntary Tax? Revisited.” USC Olin research paper 01-5. Presented at the National Tax Association’s 93rd Annual Conference on Taxation, Santa Fe, NM, November 9–11.

Task Force on Federal Wealth Transfer Taxes. 2004. Report on Reform of Federal Wealth and Transfer Taxes. Washington, DC: American Bar Association.

US Department of the Treasury. 2015. “General Explanations of the Administration’s Fiscal Year 2016 Revenue Proposals.” Washington, DC.