The federal tax code includes a range of incentives for alternatives to fossil fuels. These provisions support electricity production from solar, wind, and other renewable sources and from nuclear facilities. They also support alternative transportation fuels, especially electricity, and encourage energy efficiency in homes and commercial buildings. The Inflation Reduction Act of 2022 greatly expanded and redesigned tax incentives for alternative energy sources. However, the 2025 reconciliation bill (“One Big Beautiful Act-OBBBA”) repealed certain credits earlier than prior law, and introduced new restrictions on credit eligibility, such as excluding projects affiliated with certain foreign entities, and eliminating benefits for wind or solar energy.

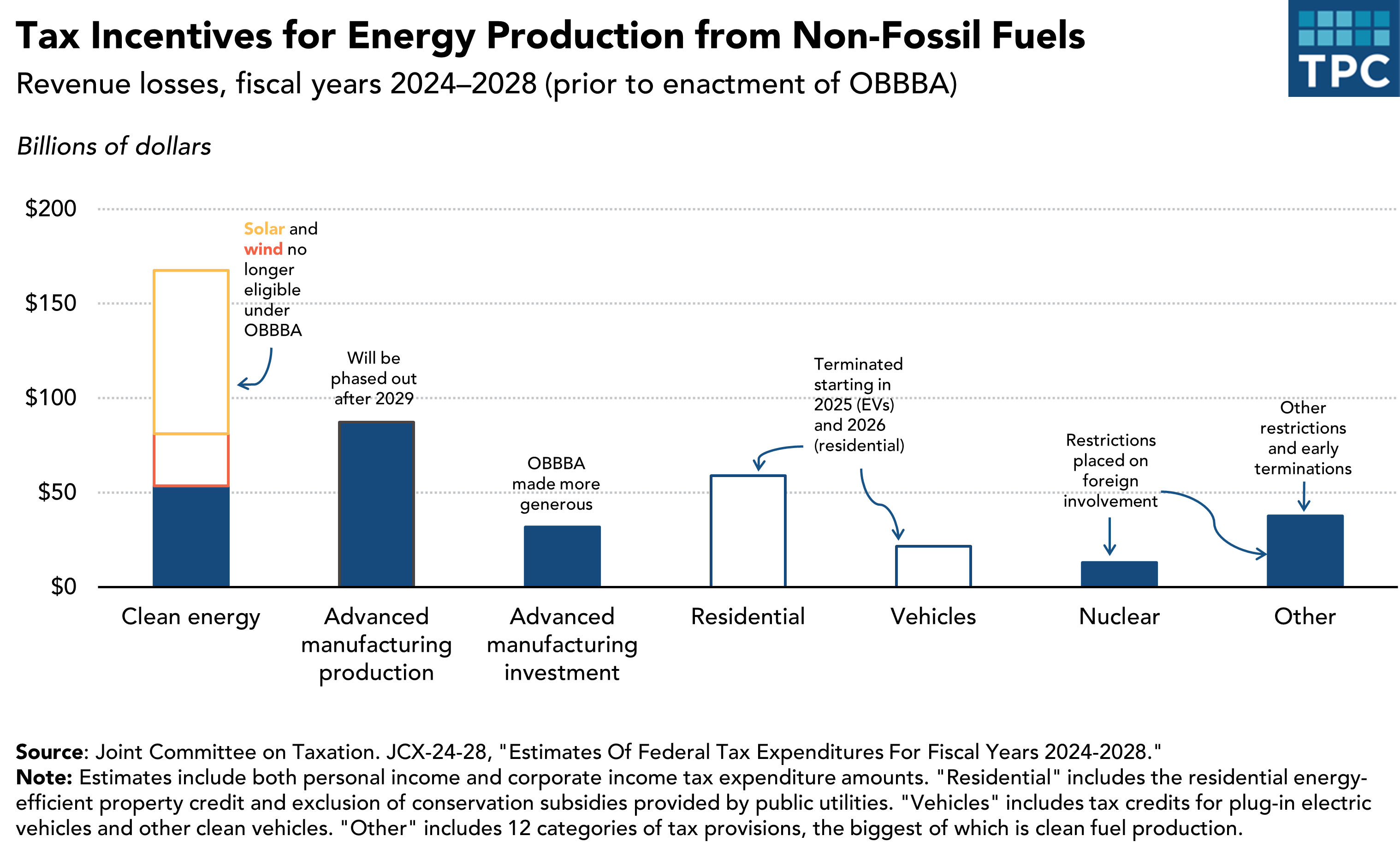

Prior to OBBBA, the federal government was projected to provide roughly $104.6 billion per year in tax subsidies that encourage non-fossil fuels (figure 1). The largest subsidies included tax credits for renewable energy sources, advanced manufacturing, and tax credits for electric vehicles.

Electricity Production

The investment tax credit (known as Section 48) provides a one-time credit for new investment in qualifying energy producing property The production tax credit (known as Section 45) provides a per kilowatt hour subsidy to qualifying facilities for the first 10 years of operation. Prior to OBBBA, solar was the primary recipient of section 45E, while wind-powered generators were the main recipients of section 45Y (see figure 1); geothermal, biomass, solid waste, and hydro facilities also qualified.

OBBBA sharply limited wind and solar projects’ eligibility for the credits: only wind and solar projects that begin construction by July 4, 2026, or are placed in service by December 31, 2027 are eligible to claim section 45Y and 48E tax credits.

New features of the Inflation Reduction Act of 2022 to sections 45 and 48 remain in effect. The new features linked the amount of the tax credit to various attributes of the energy project (Department of Energy 2023). For example, the investment tax credit was 30 percent of qualified property in 2022, before the IRA took effect. The credit now has a 6 percent base level and rises to 30 percent for projects that meet certain labor standards around prevailing wages and apprenticeship programs. An additional 10 percent is available for projects meeting domestic content standards. Projects located in energy communities also benefit from an additional 10 percent. Similar provisions apply for the production tax credit. Although the OBBBA maintains this framework, it restricts eligibility for foreign entities.

The Inflation Reduction Act also expanded support for nuclear power with a new production tax credit, which replaced two very small tax subsidies. OBBBA retained the production tax credits but introduced some new restrictions for projects by foreign entities.

The IRA introduced a new credit for clean hydrogen production. The OBBBA maintains the credit but projects must begin construction by December 31, 2027 to be eligible.

Electric Vehicles

The tax code provided a substantial tax credit to individuals and businesses who purchase or lease plug-in electric light passenger vehicles and trucks. The credit could range as high as $7,500 based on several factors, like material sourcing, domestic content, and household income (US Department of Energy). Under OBBBA, tax credits for electric vehicles were set to expire on September 30, 2025 – vehicles purchased or leased after this date are not eligible for the tax credit. Electric motorcycles previously qualified for a smaller credit, which has since expired. There are also modest credits for fuel cell vehicles and alternative refueling equipment.

Residential

The tax code also encourages homeowners to improve energy efficiency and adopt alternative sources by providing tax benefits. The largest of these benefits is the residential energy-efficient property tax credit (Section 25D), which supports home installation of solar electric and water heating systems, as well as some battery storage systems. The newly expanded residential energy efficiency credit (Section 25C) covers improvements in existing homes, including insulation upgrades and high-efficiency heating, cooling, and water heating. Under OBBBA, both sections 25C and 25D credits are scheduled to expire on December 31, 2025. Another credit for the construction of new energy-efficient homes will expire on June 30, 2026.

Energy conservation subsidies provided by public utilities are excluded from taxable income. This provision was unchanged by OBBBA.

Other

Manufacturing facilities can claim a tax credit for investment in advanced energy property that generates clean power or improves efficiency, and OBBBA permanently increased this credit. In contrast, the credit for advanced manufacturing production will gradually decline in the coming years, with ineligibility for components for wind energy or projects involving certain foreign entities.

Commercial buildings previously qualified for a special deduction for investments in lighting, heating, cooling, water heating, and building envelopes that substantially improve energy efficiency. OBBBA terminates this benefit after June 30, 2026.

The federal government also provides a financing subsidy for outstanding bonds issued to invest in renewable energy and energy conservation projects. Congress has not appropriated or authorized new clean energy bonds since they were eliminated by the Tax Cuts and Jobs Act.

Direct Pay

Tax analysts often emphasize that credits, deductions, and other tax incentives function like spending programs, which are often described as “tax expenditures.” The Inflation Reduction Act made this equivalence especially clear by allowing certain incentives—most notably the investment and production tax credits—to be claimed as direct payments by entities that do not usually pay federal income tax. Potential eligible beneficiaries of direct payment include non-profits, state and local governments, Indian Tribal governments, Alaska Native Corporations, and government-affiliated entities involved in electricity production and distribution. OBBBA retains the direct pay option wherever taxpayers remain eligible for the underlying tax benefit.

Updated October 2025

Cunningham, Lynn J. and Claire M. Jordan. 2023. “Renewable Energy and Energy Efficiency Incentives: A Summary of Federal Programs.” Washington, DC: Congressional Research Service.

Cilluffo, Anthony A., Nicholas E. Buffie, Grant A. Driessen, Jane G. Gravelle, Mark P. Keightley, Donald J. Marples, and Brendan McDermott. 2025. “Tax Provisions in P.L. 119-21, the FY2025 Reconciliation Law.” Washington, DC: Congressional Research Service.

Joint Committee on Taxation. JCX-24-28, "Estimates Of Federal Tax Expenditures For Fiscal Years 2024-2028."

US Department of Energy. 2023. “Federal Solar Tax Credits for Businesses.”

US Department of Energy. n.d. “Federal Tax Credits for All-Electric and Plug-In Hybrid Vehicles.”

White House. 2022. “Clean Energy Tax Provisions in the Inflation Reduction Act.”