The Highway Trust Fund finances most federal government spending for highways and mass transit. Revenues for the trust fund come from transportation-related excise taxes, primarily federal taxes on gasoline and diesel fuel. In recent years, however, the trust fund has needed significant transfers of general revenues to remain solvent.

The Highway Trust Fund tracks federal spending and revenue for surface transportation. The trust fund has separate accounts for highways and mass transit. Because obligations from the trust fund generally are for capital projects that take several years to complete, outlays reflect projects authorized by Congress in previous years.

Most spending from the Highway Trust Fund for highway and mass transit programs is through federal grants to state and local governments. The federal government accounts for about one-quarter of all public spending on roads and highways, with the remaining three-quarters financed by state and local governments.

Financing the Trust Fund

The Congressional Budget Office (CBO) estimates that Highway Trust Fund tax revenue will total $43 billion in fiscal year 2023 (figure 1). Revenue from the federal excise tax on gasoline ($25.0 billion) and diesel fuel ($10.8 billion) accounts for 83 percent of the total. The remaining trust fund tax revenue comes from a sales tax on tractors and heavy trucks, an excise tax on tires for heavy vehicles, and an annual use tax on those vehicles. In addition to dedicated tax revenue, the trust fund receives a small amount of interest on trust fund reserves.

The current tax rates are 18.4 cents per gallon for gasoline and ethanol-blended fuels and 24.4 cents per gallon for diesel (0.1 cent of each tax is dedicated to the Leaking Underground Storage Tank Trust Fund). The tax rates on motor fuels have not changed since 1993 and thus have failed to keep pace with inflation. If tax rates had been indexed for inflation since 1993, the current tax on gasoline would be about 37 cents per gallon and the tax on diesel fuel would be about 49 cents per gallon. Although the current taxes on motor fuels (except for a residual tax of 4.3 cents per gallon) are set to expire at the end of September 2028, Congress has routinely extended the taxes in the past.

Trust Fund Balances

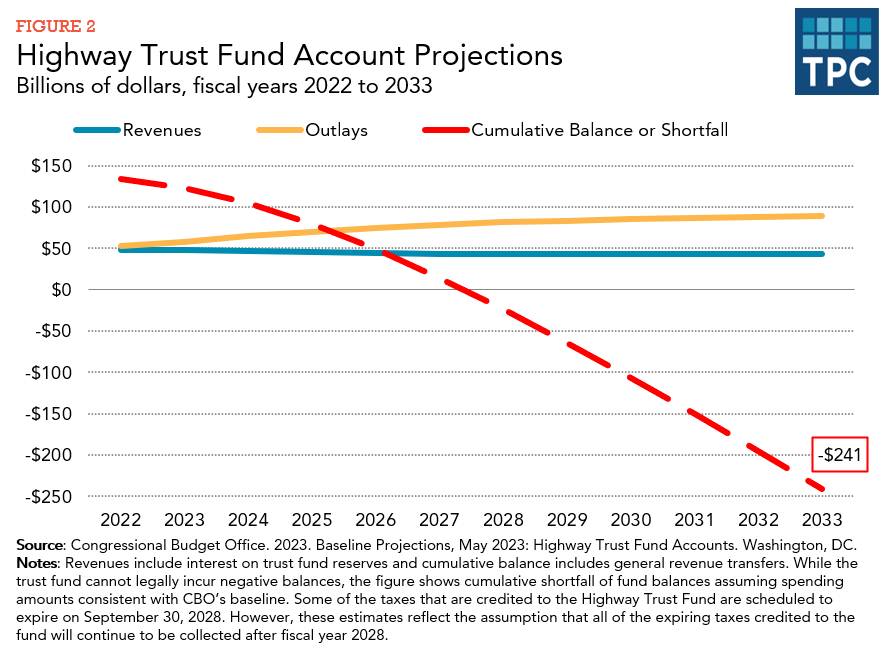

Before 2008, highway tax revenue dedicated to the trust fund was sufficient to pay for outlays from the fund, but that has not been true in recent years. Since 2008, Congress has transferred general revenues to the fund on numerous occasions including $118 billion in the Infrastructure Investments and Jobs Act of 2021.

Those transfers will enable the trust fund to meet spending obligations through 2027, but projected shortfalls will appear again by the end of 2028 (figure 2). The Congressional Budget Office projects that, by 2033, outlays from the Highway Trust Fund will exceed trust fund reserves by a cumulative $181 billion for the highway account and by $60 billion for the mass transit account, even if expiring trust funds taxes are extended (CBO 2023).

Financing Federal Spending on Highways and Mass Transit

Congress could pay for projected highway and mass transit spending by simply raising the federal tax rate on gasoline and diesel fuel. Increasing those rates by 15 cents per gallon along with indexing the rates for inflation would increase federal revenues by $240 billion over ten years (CBO 2022). (The increase in revenues for the trust fund would be greater than $240 billion because the revenue estimate includes the negative impact of higher fuel taxes on federal income and payroll taxes. Higher motor fuels taxes would increase costs for businesses, thus lowering business profits, employee wages, and the federal taxes collected on that income.)

Drivers likely would respond to an increase in motor fuels taxes by driving less, which would reduce pollution and lessen the need for highway construction and maintenance. But drivers may also respond by driving more fuel-efficient vehicles, which would weaken the incentive to reduce miles driven.

Motor fuels taxes link highway use with the associated costs of building and maintaining roads as well other costs associated with fuel consumption, such as pollution and dependence on foreign oil. But motor fuels taxes are an imperfect user fee because they do not differentiate among vehicles that cause greater or lesser road wear for the same amount of fuel consumed or between travel on crowded and uncrowded roads.

A tax on vehicle miles driven would provide a more direct link to the cost of highway use but, unlike an increase in the tax on motor fuels, would be difficult to implement, requiring new tolls or electronic motoring of vehicles. An advantage of a vehicle mileage tax is that it could adjust to reflect the additional costs of congestion by increasing tolls or the tax rate in certain locations and at certain times of the day. A vehicle mileage tax would not, however, provide an incentive for driving more fuel-efficient vehicles.

Alternatively, Congress could abandon the user-pay principle and simply pay for highways through general revenues. Highway spending would no longer have a dedicated source of revenue and would instead compete with other spending programs for general revenue funding through the annual appropriations process. Or Congress could decide to limit federal highway spending to the amount of revenue collected from existing motor fuels taxes. This would require curtailing some existing highway projects and not starting others, at a time when the nation’s infrastructure is already in need of repair.

Updated January 2024

Congressional Budget Office. 2014. The Highway Trust Fund and the Treatment of Surface Transportation Programs in the Federal Budget. Washington, DC.

Joint Committee on Taxation. 2015. Long-Term Financing of the Highway Trust Fund. JCX-92-15. Washington, DC.

Kile, Joseph. 2015. Testimony on the Status of the Highway Trust Fund and Options for Paying for Highway Spending. Testimony before the US Senate Committee on Finance, Washington, DC, June 18.

Kirk, Robert S. and William J. Mallet. 2019 Funding and Financing Highways and Public Transportation. R45350. Washington, DC: Congressional Research Service.

Peter G. Peterson Foundation. 2023. The Highway Trust Fund Explained. Washington, DC.