Many preferences in the tax code phase out for high-income taxpayers—their value falls as income rises. Phaseouts target tax benefits to low- and middle-income households while limiting revenue costs, but raise marginal tax rates for taxpayers in the phase-out range.

Many preferences in the tax code phase out for higher-income taxpayers, meaning their value declines after income reaches a certain level. Phaseouts target tax benefits on middle- and lower-income households and limit the loss of revenue. Phaseouts, however, not only claw back benefits from the more affluent, but also increase the effective marginal tax rate these taxpayers face, decreasing the after-tax gains of earning more income.

Some taxpayers are affected by multiple tax provisions phasing out at the same time, compounding the negative impact on their earning incentives. More broadly, phaseouts complicate the tax code and make taxes more difficult to understand.

How Do Phaseouts Work?

Phaseouts are structured in different ways and thus have different effects. Some reduce credits and thus have the same impact on all affected taxpayers. Others reduce deductions, in which case their dollar impact depends on the taxpayer’s marginal tax rate: the higher the tax rate, the greater the value of the lost deduction.

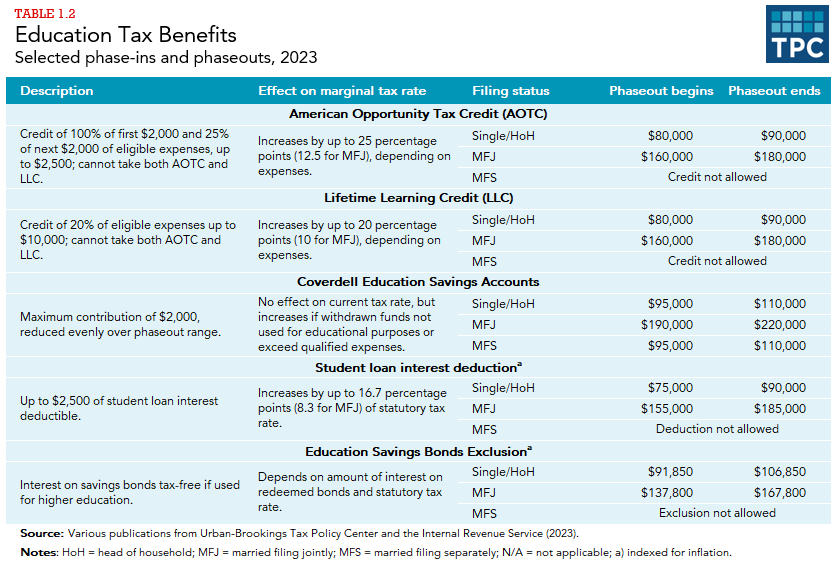

Phaseouts reduce tax benefits at different rates depending on their structure and range. Most phaseouts reduce benefits at a constant rate over an income range; that rate depends on the width of the range. For example, for single tax filers, the American Opportunity Tax Credit phases out evenly over a $10,000 range, so the maximum $2,500 credit phases out at a 25 percent rate ($25 per $100 of income above the phaseout thresholds). In contrast, the adoption credit, in tax year 2023, phases out over a $40,000 range between incomes of $239,230 and $279,230, so the maximum $15,950 credit phases out at about a 35 percent rate ($35.75 per $100 of income above the threshold).

Some phaseouts, however, reduce benefits by a specified amount for each fixed increment of income. For example, the child tax credit decreases by $50 for every $1,000 or part of $1,000 in additional income above the phaseout threshold. Whether income exceeds the threshold by $1 or by $999, the credit falls by the same $50, so earning a few more dollars could make a taxpayer worse off.

Some phaseouts have more pronounced cliffs, so the benefit drops in large increments when income exceeds the threshold.

Many phaseouts are indexed for inflation so that the phaseout ranges remain fixed in real terms. Phaseouts that are not adjusted for inflation affect more taxpayers over time, as inflation raises nominal incomes and thus lifts more taxpayers above the phaseout thresholds.

In addition to phaseouts, the tax code also contains phase-ins. For example, a portion of Social Security benefits becomes taxable only when a taxpayer’s income reaches certain thresholds, and the taxable portion increases (up to a maximum of 85 percent) as the amount by which income exceeds those thresholds increases.

Where are Phaseouts Most Common?

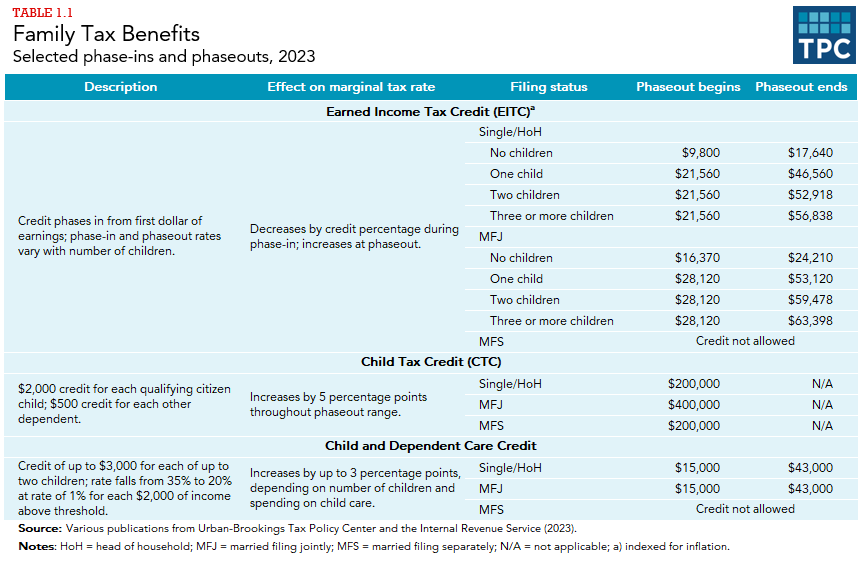

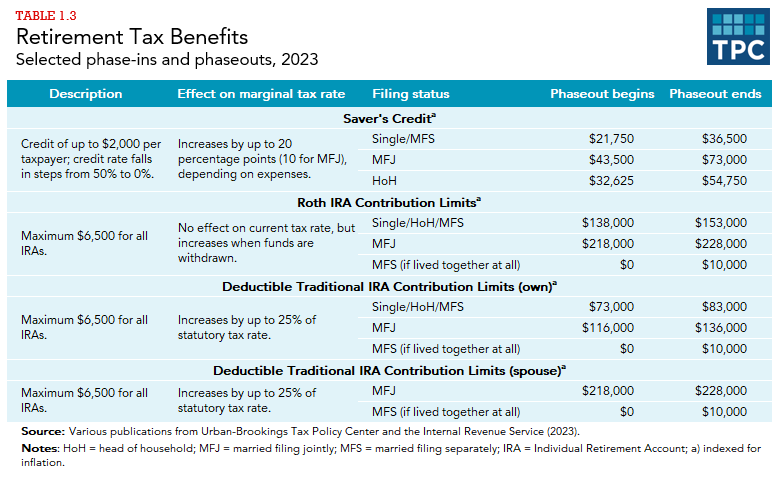

Phaseouts are most common in three areas of the tax code: family benefits, education provisions, and retirement savings provisions (table 1). The beginning and ending points of the phaseout range determine who is eligible for these credits or deductions. For example, for 2023, the earned income tax credit (EITC) begins to phase out at income of $21,560 for single parents and at $28,120 for married couples with one child, limiting EITC eligibility to low-income families. In contrast, the child tax credit (CTC) begins to phase out at income of $200,000 for single parents and at $400,000 for married couples with children, extending CTC eligibility to high-income families.

Phaseouts can Create Marriage Bonuses and Penalties

Phaseouts can create both marriage bonuses and penalties. A marriage bonus reduces a couple’s combined tax bill compared to what they would pay if they were not married and filed separate returns. For example, in tax year 2023, phaseout of the CTC begins at $400,000 for married taxpayers and $200,000 for all other taxpayers. If one spouse in a couple with a child has $300,000 of income and the other has none, their combined income is under the joint filers’ threshold for phaseout of CTC and they can claim a child tax credit. If they were not married, the higher-income spouse could not claim the CTC because his or her income was too high, and the lower-income spouse could not claim the credit because he or she had no income.

Before the TCJA, married couples faced significant marriage penalties because their phaseout range was less than twice that for single tax filers. Under TCJA, most phaseouts for joint filers are exactly twice that for single filers, so many of the marriage penalties are gone.

However, phaseouts still impose marriage penalties on low-income families, and those penalties are often a larger percentage of income than the marriage penalties caused by phaseouts for higher-income taxpayers.

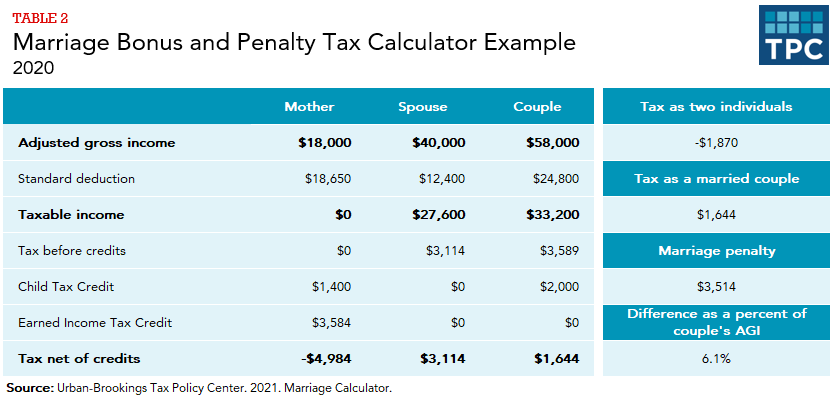

For example, in 2020, a single mother who earned $18,000 and had one child paid no income tax and received two refundable credits—a $1,400 CTC and a $3,584 EITC (table 2). (In 2020, a single parent with one child paid income tax (before credits) when their income exceeded $18,650—the standard deduction for a head of household.) If she married her partner making $40,000—whose 2020 income tax as a single person was $3,114—she would have lost all her EITC (the couple’s income would cause the credit to phase out completely) but would have gotten more CTC. (In 2020, CTC was worth up to $2,000 per qualifying child. The refundable portion of the credit was limited to $1,400.) Losing the EITC would mean that the couple would have paid $1,644 in income tax when married, compared with receiving a net payment of $1,870 (her $4,984 combined credit minus her partner’s $3,114 tax) if they remained single. That difference is a marriage penalty of $3,514, or 6.1 percent of the couple’s adjusted gross income.

Updated January 2024

Gale, William G. 2001. “Tax Simplification: Issues and Options.” Testimony before the House Committee on Ways and Means, Washington, DC, July 17.