What is the child tax credit?

The child tax credit provides a credit of up to $2,000 per child under age 17. If the credit exceeds taxes owed, families may receive up to $1,600 per child as a refund. Other dependents—including children ages 17–18 and full-time college students ages 19–24—can receive a nonrefundable credit of up to $500 each.

How the CTC Works Today

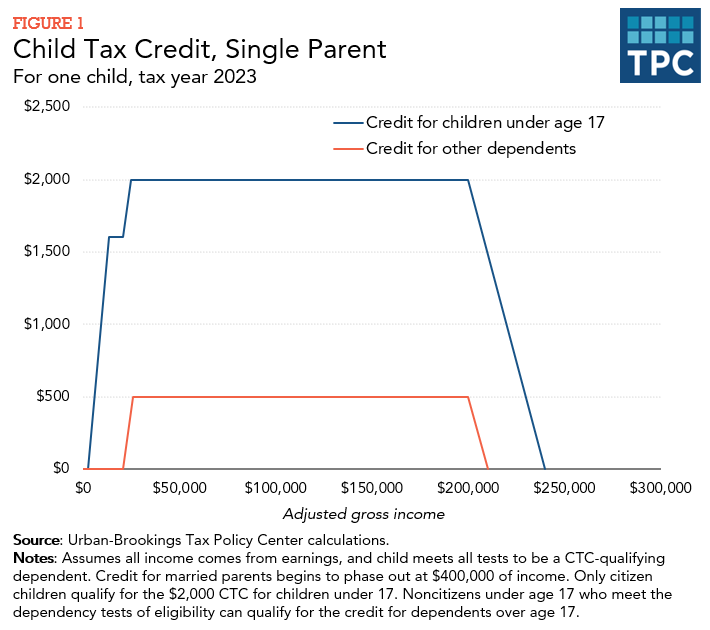

Taxpayers can claim a child tax credit (CTC) of up to $2,000 for each child under age 17 who is a citizen. The credit is reduced by 5 percent of adjusted gross income over $200,000 for single parents ($400,000 for married couples). If the credit exceeds taxes owed, taxpayers can receive up to $1,600 of the balance as a refund, known as the additional child tax credit (ACTC) or refundable CTC. The ACTC is limited to 15 percent of earnings above $2,500 (figure 1).

For the most part, the CTC is not indexed for inflation. The exception to this is the amount of the credit families with children under 17 can receive as a refund. This amount (which was set at $1,400 in 2018) will increase annually with inflation until it becomes equal to the full value of the credit ($2,000). In 2030, the refundable portion of the credit is $1,600. The refundable portion increases in $100 increments with inflation.

Starting in 2018, a $500 credit was made available to dependents who were not eligible for the $2,000 CTC for children under 17 (figure 1). Before 2018, these individuals would not have qualified for a tax credit but would have qualified for a dependent exemption, which was eliminated by the 2017 Tax Cuts and Jobs Act (TCJA). Dependents eligible for this credit include children ages 17–18 or those 19–24 and in school full time in at least five months of the year. Also included are older dependents—representing about 6 percent of dependents eligible for the CTC.

After 2025, the CTC is scheduled to revert to its pre-TCJA form. At that point, taxpayers will be able to claim a credit of up to $1,000 for each child under age 17 and the credit will be reduced by 5 percent of adjusted gross income over $75,000 ($110,000 for married couples). If the credit exceeds taxes owed, taxpayers will be able to receive the balance as a refund (the ACTC). The ACTC will be limited to 15 percent of earnings above $3,000.

Impact of the CTC

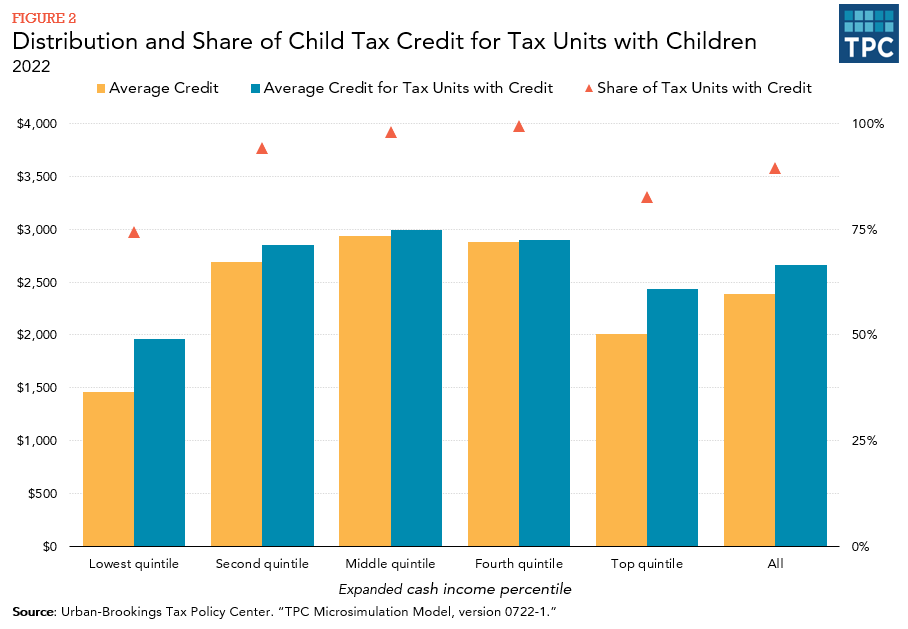

The Tax Policy Center estimates that 90 percent of families with children received an average CTC of $2,390 in 2022 (the average credit can exceed the maximum per child credit because families can have more than one child). Families with children in all income groups benefited from the CTC, but families in the lowest income quintile were least likely to benefit from the credit because more of them will not have sufficient earnings to qualify for the credit. Just under three-quarters of families in the lowest income quintile were eligible for a CTC, receiving an average credit of $1,460. The average credit was the smallest for this quintile because low-income families are most likely to be limited to the refundable portion of the credit, which was capped at $1,500 in 2022 rather than the full $2,000 limit for the nonrefundable credit (figure 2).

The percentage of families with children receiving the credit and the average credit received were the highest among moderate- and middle-income families. The share of of families with children claiming a CTC was 94 percent in the second income quintile, 98 percent in third quintile, and 99 percent in the fourth quintile. The proportion of families with children receiving a credit then drops to 90 percent in the highest income quintile because of the phase-out of the credit at high incomes (figure 2).

The CTC has a significant impact on the economic well-being of low-income families with children. If the official estimate of poverty counted the CTC as income (including the refundable portion), 4.3 million fewer people would have fallen below the federal poverty line in 2018, including about 2.3 million children. Counting the credit would have also reduced the severity of poverty for an additional 12 million people, including 5.8 million children (Center on Budget and Policy Priorities 2019).

Recent History of the CTC

The American Rescue Plan Act (ARPA) increased the Child Tax Credit (CTC) for tax year 2021. Tax filers could claim a CTC of up to $3,600 per child under age 6 and up to $3,000 per child ages 6 to 17. There was no cap on the total credit amount that a filer with multiple children could claim. The credit was fully refundable – low-income families could qualify for the maximum credit regardless of how little they earned. If the credit exceeded taxes owed, families could have received the excess amount as a tax refund.

Only children who are US citizens were eligible for these benefits. The credit phased out in two steps. First, the credit began to decrease at $112,500 of income for single parents ($150,000 for married couples), declining in value at a rate of 5 percent of adjusted gross income over that amount until it reached pre-2021 levels. Second, the credit’s value was further reduced by 5 per-cent of adjusted gross income over $200,000 for single parents ($400,000 for married couples) (figure 1, blue lines).

Prior to the ARPA, the CTC had been changed in the Tax Cuts and Jobs Act (TCJA) of 2017. Effective in the 2018 the TCJA doubled the CTC for children under 17 from $1,000 per child to $2,000 per child. The legislation specified in 2018 that up to $1,400 of the credit could be received as a refundable credit. The refundable amount was indexed to inflation. Only children who are US citizens were eligibile for this credit. The legislation also allowed dependents who do not qualify for the $2,000 credit to qualify for a nonrefundable credit worth up to $500. The legislation is temporary and expires after 2025. At that point, the credit for children under 17 will revert to $1,000 per child, and other dependents will no longer be eligible for a CTC.

Before these changes, the American Taxpayer Relief Act of 2012 had increased the CTC from $500 per child, its pre-2001 level, to $1,000 per child. It also temporarily extended the provisions of the American Recovery and Reinvestment Act of 2009 (the anti-recession stimulus package) that reduced the earnings threshold for the refundable CTC from $10,000 (adjusted for inflation starting after 2002) to $3,000 (not adjusted for inflation). The Bipartisan Budget Act of 2015 made the $3,000 refundability threshold permanent. The TCJA further reduced the refundability threshold to $2,500 starting in 2018, but that lower threshold will expire after 2025 when the $3,000 refundability threshold will return.

The refundable CTC was originally designed in 2001 to coordinate with the earned income tax credit (EITC). Once earnings reached $10,020 for families with two children in 2001, there was no further increase in the EITC. The earnings threshold for the refundable CTC was set at $10,000 so families could now receive a subsidy for earnings in excess of that amount. Like the earning threshold amounts for the EITC, the $10,000 earnings threshold was indexed for inflation. When the earnings threshold for the refundable CTC was reduced—first to $8,500 in 2008 and then to $3,000 in 2009—that link between the phase-in of the refundable CTC and the EITC was broken.

Updated January 2024

Urban-Brookings Tax Policy Center. “TPC Microsimulation Model, version 0722-2.” Washington, DC.

Center on Budget and Policy Priorities. 2023. “Policy Basics: The Child Tax Credit.” Washington, DC.

Maag, Elaine. 2019. “Shifting Child Tax Benefits in the TCJA Left Most Families About the Same.” Washington, DC: Urban Institute.

Maag, Elaine. 2018. “Who Benefits from the Child Tax Credit Now?.” Washington, DC: Urban-Brookings Tax Policy Center.

Maag, Elaine. 2016. “Reforming the Child Tax Credit: An Update.” Washington, DC: Urban-Brookings Tax Policy Center.

Maag, Elaine. 2015. “Reforming the Child Tax Credit: How Different Proposals Change Who Benefits.” Washington, DC: Urban Institute.

Maag, Elaine. 2013. “Child-Related Benefits in the Federal Income Tax.” Washington, DC: Urban-Brookings Tax Policy Center.

Maag, Elaine, and Lydia Austin. 2014. “Implications for Changing the Child Tax Credit Refundability Threshold.” Tax Notes. Washington, DC.

Maag, Elaine, and Julia B. Isaacs. 2017. “Analysis of a Young Child Tax Credit: Providing an Additional Tax Credit for Children under 5.” Washington, DC: Urban-Brookings Tax Policy Center.

Maag, Elaine, Stephanie Rennane, and C. Eugene Steuerle. 2011. “A Reference Manual for Child Tax Benefits.” Washington, DC: Urban-Brookings Tax Policy Center.