Are federal taxes progressive?

Overall, yes. But that’s not the case for each tax.

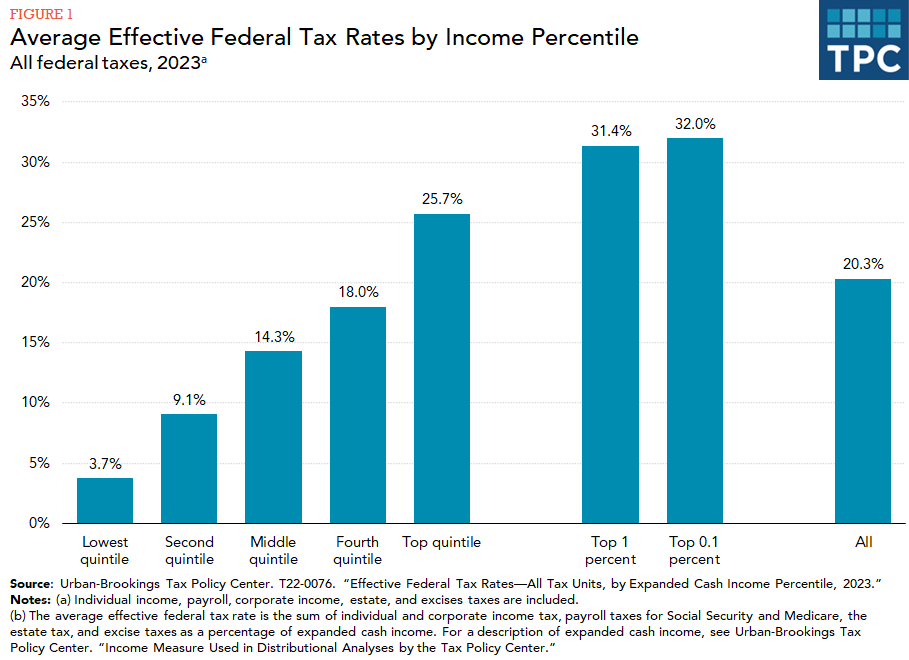

The overall federal tax system is progressive, with total federal tax burdens a larger percentage of income for higher-income households than for lower-income households.

Not all taxes within the federal system are equally progressive and some federal taxes are regressive, as they make up a larger percentage of income for lower-income than for higher-income households.

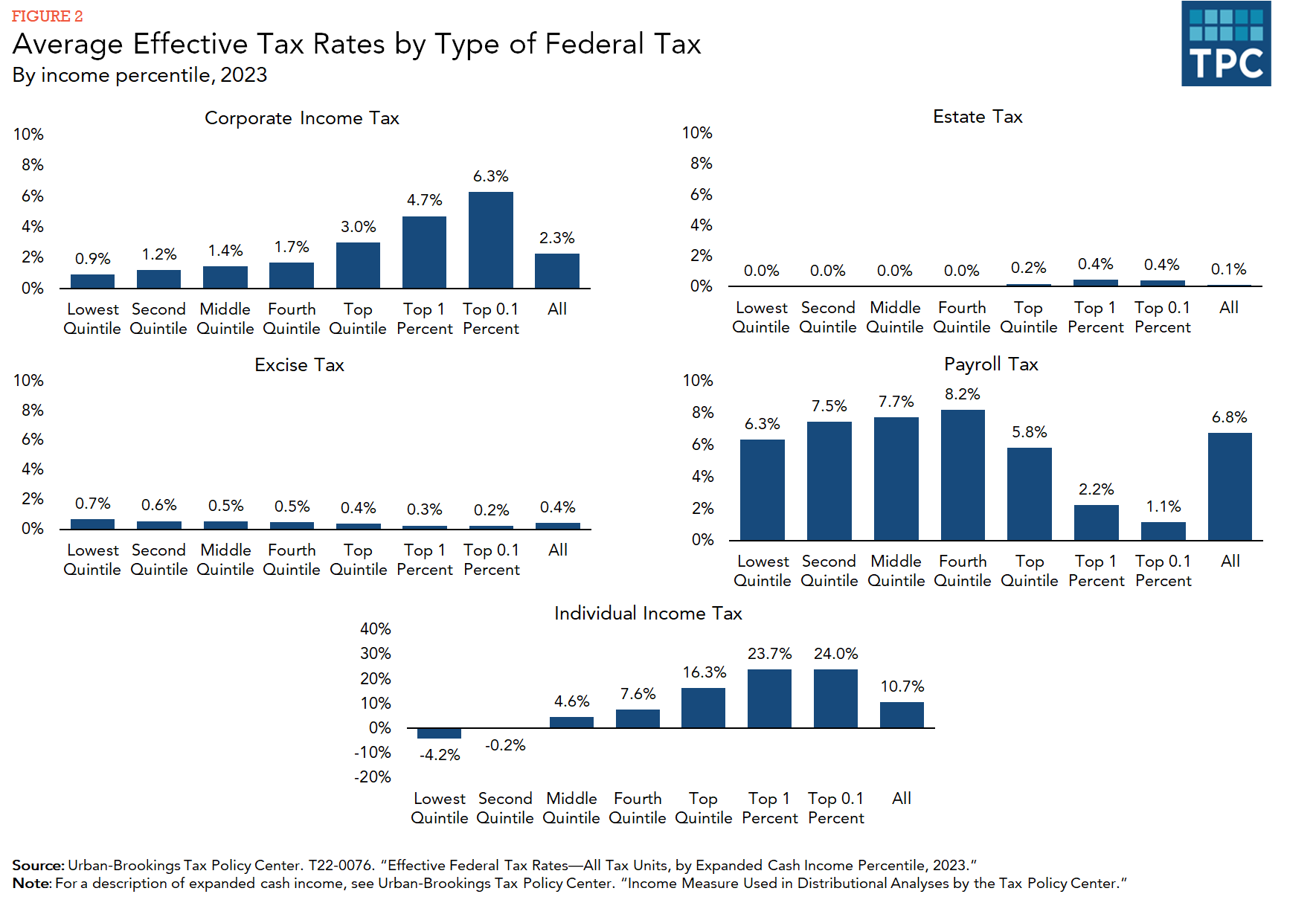

The individual and corporate income taxes and the estate tax are progressive. By contrast, excise taxes are regressive and payroll taxes for Social Security and Medicare are regressive at the top of the income distribution (see figure 2).

Individual income tax

The individual income tax is progressive, thanks to the impact of refundable credits for lower-income households (average tax rates are negative for the two lowest income quintiles), the standard deduction (which exempts a minimum level of income from the tax), and a graduated rate structure (rates on ordinary income rise from 10 to 37 percent, with an additional 3.8 percent marginal tax on certain investment income of high-income households). Various tax preferences, including those for capital gains, retirement saving, and home mortgage interest, make the income tax less progressive than it would otherwise be.

Corporate income tax

The corporate income tax is progressive because most of its burden falls on income from dividends, capital gains, and other forms of capital income disproportionately received by high-income households.

ESTATE TAX

The estate tax is only imposed on households with high levels of wealth. Only wealth above an exemption amount is subject to the tax—that amount for those who die in 2023 is $12.92 million, and it is effectively double that amount for married couples. High wealth is almost always commensurate with high income, so, when households are classified by income, virtually the entire estate tax burden falls on the very highest income households.

PAYROLL TAXES

The regressive nature of payroll taxes stems from two factors. First, the Social Security portion of payroll taxes is subject to a cap: in 2023, individuals will pay the tax on only their first $160,200 in earnings. Second, compared with lower-income households, higher-income households receive more of their income from sources other than wages, such as capital gains and dividends, which are not subject to the payroll tax. However, because wages rise as a share of income over the first four quintiles of the distribution, payroll taxes are slightly progressive until high income levels are reached.

Excise taxes

An excise tax increases the price of the taxed good or service relative to the prices of other goods and services. Households that consume more of the taxed good or service as a share of their total consumption face more of the tax burden from this change in relative prices All consumption taxes, including selective excise taxes also effectively exempt the normal return to capital, which is received mostly by upper income households.. The regressivity of most current federal excise taxes results from both the exemption of normal returns to capital and of the relative price effect, because, on average, major taxed goods, such as alcohol and tobacco products, represent a declining share of consumption as household income rises.

Updated January 2024

Urban-Brookings Tax Policy Center. 2022. T22-0075. “Average Effective Federal Tax Rates—All Tax Units, by Expanded Cash Income Level, 2023”; and T22-0076. “Effective Federal Tax Rates—All Tax Units, by Expanded Cash Income Percentile, 2023.”

Burman, Leonard E. 2007. “Fairness in Tax Policy.” Testimony before the Subcommittee on Financial Services and General Government, House Appropriations Committee, Washington, DC, March 5.

Joint Committee on Taxation. 2015. “Fairness and Tax Policy.” JCX-48-15. Washington, DC: Joint Committee on Taxation.

Urban-Brookings Tax Policy Center. “Income Measure Used in Distributional Analyses by the Tax Policy Center.”