The voices of Tax Policy Center's researchers and staff

The New York Times reports that some Republican senators are clamoring for larger tax cuts, especially for pass-through business income. The Times says that while the GOP leadership is looking to increase rewards for high-income business owners, there is little momentum for amendments to increase tax cuts for low-income Americans.

These complaints might seem odd to critics who view the versions of the Tax Cut and Jobs Act (TJCA) moving through Congress as too costly in an era of rising federal debt and too generous to high-income taxpayers. Yet people often link their judgments about legislation to their expectations. And some Republicans in Congress and their supporters may legitimately believe that the TJCA falls far short of what they were promised by their presidential candidates in the last election.

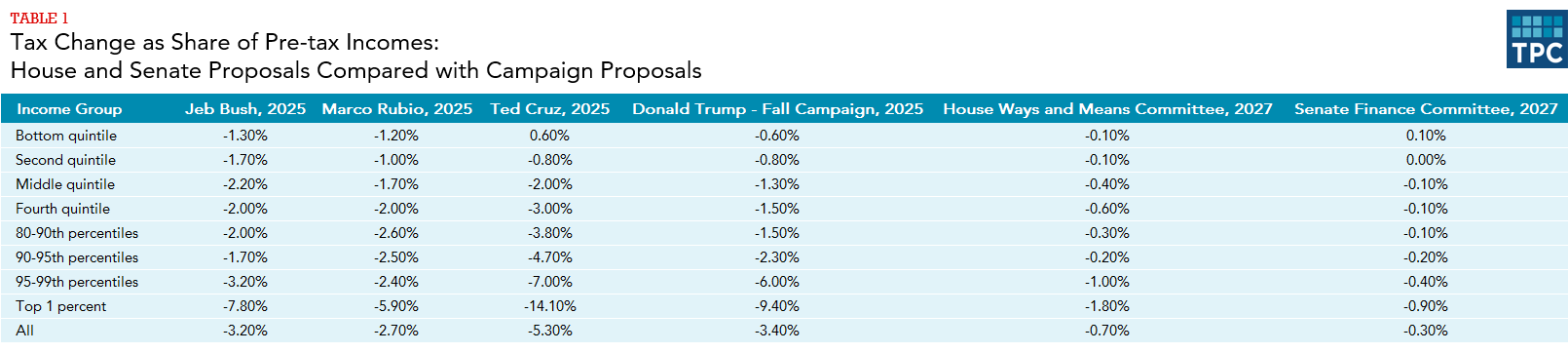

I created a table that shows the Tax Policy Center’s estimates of how much four leading Republican presidential candidates proposed to cut taxes as a share of pre-tax income. Then I compared these estimates with TPC’s estimates for the House and Senate Finance Committee versions of the TJCA. I used the latest year for which TPC provided estimates – 2025 for the candidates’ proposals and 2027 for the House and Senate bills. The Senate Finance Committee proposal reflects the repeal of individual income tax cuts to achieve revenue neutrality by 2027; TPC still shows a small total tax reduction because its estimates do not include the net reduction in the budget deficit from the repeal of the Affordable Care Act’s individual health insurance mandate.

The House-passed TCJA would, in 2027, cut taxes by 0.7% of pre-tax income while the Senate bill would reduce taxes by 0.3% of income. But in the 2016 campaign, Marco Rubio proposed tax cuts equal to 2.7% of income while Ted Cruz would have cut taxes by 5.3% of income (both for 2025, about a decade into the future). Donald Trump’s fall 2016 proposals, scaled back from his earlier plans, would have reduced taxes by 3.4% of income (also for 2025).

Their proposed tax cuts for those at the top of the income scale (also a decade into the future) were even greater. For the top 1 percent, Cruz would have cut taxes by 14.1% of pre-tax income, Rubio promised to cut taxes by 5.9% of income, and Trump vowed tax cuts equal to 9.4% of income. In comparison, the House and Senate proposals, while disproportionately beneficial to the top 1 percent, would reduce the tax burdens of this income group by only 1.8% of income (House) and 0.9% of income (Senate), about a decade after enactment.

This is not to say that tax legislation should either increase the federal budget deficit or provide the largest tax cut as a share of income to the highest income taxpayers. But it is worth noting how far the Congressional proposals have moved from where the Republican presidential candidates, including the election winner, started out.

Matt Rourke/AP Photo