The voices of Tax Policy Center's researchers and staff

Tax-based aid for higher education quadrupled between 2000 and 2010 and will continue to be a large part of the financial aid story – at least through 2017 when the American Opportunity Tax Credit is scheduled to expire. As part of a series of reports on federal financial aid, the Center for Law and Social Policy is urging a full review of who receives tax benefits for education, how those benefits compare with the better-known Pell grants, and whether Congress should reform higher education benefits. It proposes some important ideas for better targeting those subsidies to students who need them the most.

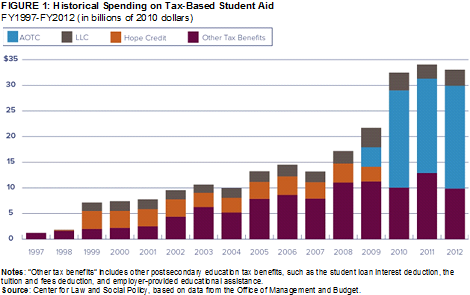

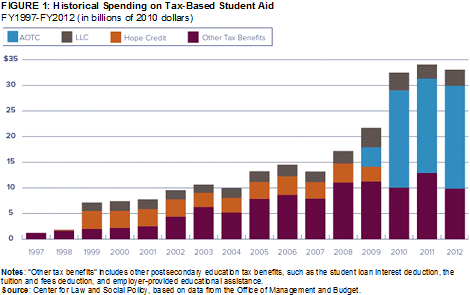

Since the enactment of the Hope and Lifetime Learning Credits in 1997, education tax benefits have grown from less than $1 billion to over $34 billion in FY2012. Most of that growth comes from the AOTC, which replaced the Hope credit in 2009 (figure 1).

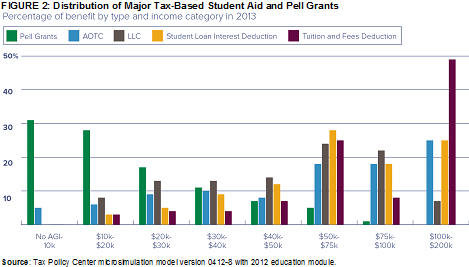

In 2012, the $34.2 billion in tax-based aid represented nearly half of all non-loan federal assistance and rivaled the $35.6 billion in Pell grants. But unlike Pell grants that assist low-income students, tax subsidies often benefit students who are already likely to attend college. The Tax Policy Center estimates that in 2013, a quarter of the aid from the AOTC and half of the aid from the tuition and fees deduction will go to students in families with incomes between $100,000 and $200,000 (figure 2). According to the National Center for Education Statistics, in 2010 barely half of students from low-income families enrolled in two- or four-year colleges immediately after completing high school. In contrast, two-thirds of kids from middle-income families and 82 percent of kids from households making $100,000 or more went straight to college.

In addition, under current rules, tax aid often comes too late to be useful for low-income students. Unlike Pell grants which provide benefits at enrollment, tax benefits typically come when a person files their tax return – something that can happen more than a year after a student needs to pay tuition.

Experts have long noted the need to reform tax-based aid, and the CLASP report offers up some solutions. CLASP suggests three ways to better target tax subsidies to those students most in need and least likely to attend college. They focus on increasing the value of the AOTC for low-income families, simplifying the tax-based aid system by eliminating credits and deductions for those likely to go to college absent the tax benefits, and piloting real-time payment of the AOTC.

The CLASP proposal would improve both the efficiency and effectiveness of the tax incentives. However, even with these reforms, tax benefits may never help poor students as well as direct assistance like Pell grants.