Brief

Tax Debate 2017

April 20, 2017

This year, Congress will consider what may be the biggest tax bill in decades. This is one of a series of briefs the Tax Policy Center has prepared to help people follow the debate. Each focuses on a key tax policy issue that Congress and the Trump administration may address.

The election of President Trump and continued Republican control of Congress has increased the likelihood of a significant tax bill in 2017. Whether Congress enacts broad structural reform or a tax cut remains an open question, but understanding the fiscal environment in which this debate will occur is important.

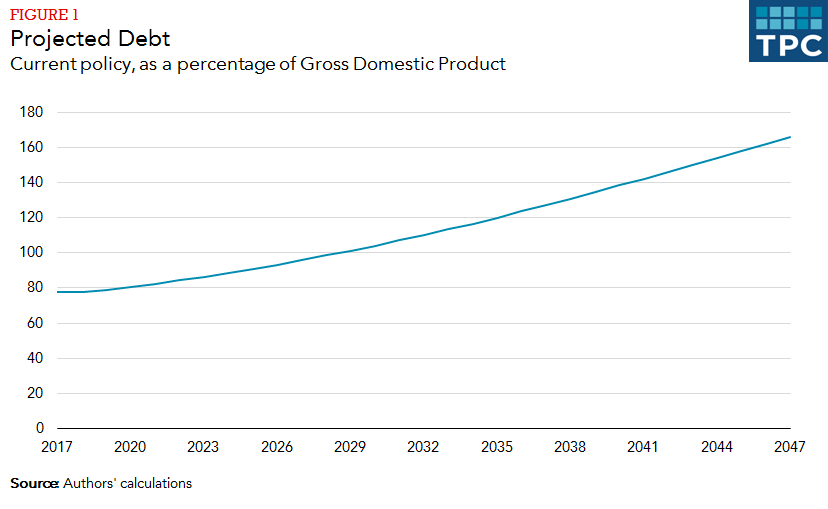

At the beginning of 2017, the federal debt was equal to 77 percent of the US economy, the largest share it has been since World War II. Further, the first of roughly 77 million baby boomers reached retirement age in the last few years, meaning spending on Social Security and Medicare will increase for decades to come as the ranks of retirees swell in numbers.

Our most recent estimates with UC Berkeley economist Alan Auerbach project that under current policy, the debt will rise to 96 percent of gross domestic product (GDP) by 2027 and 166 percent by 2047 (figure 1). We also estimate that the annual budget deficit will increase from 2.9 percent of GDP in 2017 to 6.1 percent of GDP by 2027 and to 10.5 percent of GDP by 2047.

Those projections incorporate data from the most recent Congressional Budget Office long-term budget outlook and assume that taxes and spending follow usual patterns. The projections also assume that Social Security and Medicare continue to pay all scheduled benefits even though their trust funds lack the money to do so at some point in the future. Unlike the Congressional Budget Office baseline, however, we assume that all temporary tax provisions will be extended indefinitely.

Our estimates are uncertain. They may be too optimistic because they assume the economy will remain near full employment and we will fight no new wars over the next 30 years. Other factors, such as lower-than-expected interest rates or muted growth in health care spending, could make them too pessimistic. Almost all plausible scenarios, however, project that debt will rise relative to the economy over the next few decades because of the spending pressure created by the aging population.

Rising public debt will crowd out investment and stymie long-term growth. In an economy in which all resources are already utilized, the economy expands by raising its capacity—by investing more in plants, equipment, software, and human capital. In such circumstances, theory and evidence show, the increase in borrowing created by a growing deficit will crowd out other private investment, reduce national saving, and limit the economy’s ability to expand. Those effects occur incrementally, but they are real and sizable. Consequently, sustained deficits and rising debt slowly reduce future living standards relative to what they otherwise would have been.

Besides its direct economic effects, high and rising debt can cause other problems. It can constrain policymakers by reducing the fiscal flexibility that is needed during emergencies or economic downturns. It may also limit government options during normal economic times by making the budget more sensitive to interest rates and inflation (which raises interest rates). And even if it does not directly cause a financial crisis, a high debt level may make the economy more susceptible to a financial crisis from other sources and make it harder for the government to respond.

Such fiscal risks suggest that tax reform should raise either the same amount or more revenue than does current law. We do not have fiscal room for substantial tax cuts nor do we need them given our relatively strong economy.

President Trump and the House Republicans, however, have proposed tax plans that, according to Tax Policy Center and Penn-Wharton Budget Model estimates, would reduce revenue by $6.0 trillion and $2.5 trillion, respectively, over a decade (even after accounting for those plans’ effects on economic growth). When interest costs are included, the two plans would increase the debt by $7.0 trillion and $3.0 trillion, respectively, over a decade.

Some Congressional leaders, including Speaker Paul Ryan, have suggested that legislators will enact revenue-neutral reform. Moreover, President Trump has claimed that economic growth would reduce the cost of his most recent tax plan to $2.6 trillion and that those revenue losses would be recouped through spending reductions, higher exports, new incentives for production of domestic energy, and regulatory reform.

It is unclear how policymakers will strike a deal in today’s political environment, especially given their recent failed efforts in health care policy. Financial markets currently seem relatively unconcerned about these fiscal prospects, but that could change abruptly.