The Tax Policy Center (TPC) generally produces estimates relative to a “current law” baseline. Current law refers to tax laws that will prevail if Congress does not act to change them. This includes tax provisions that change or expire over time. The definition of current law will typically change when Congress enacts legislation that affects the tax code.

TPC’s baseline is not a forecast of future outcomes. Rather, it is a benchmark projecting what the economy, federal revenues, and federal spending would look like under current law. That provides a consistent framework for evaluating how different policy options would affect the federal budget, tax burdens, and the distribution of taxes across households.

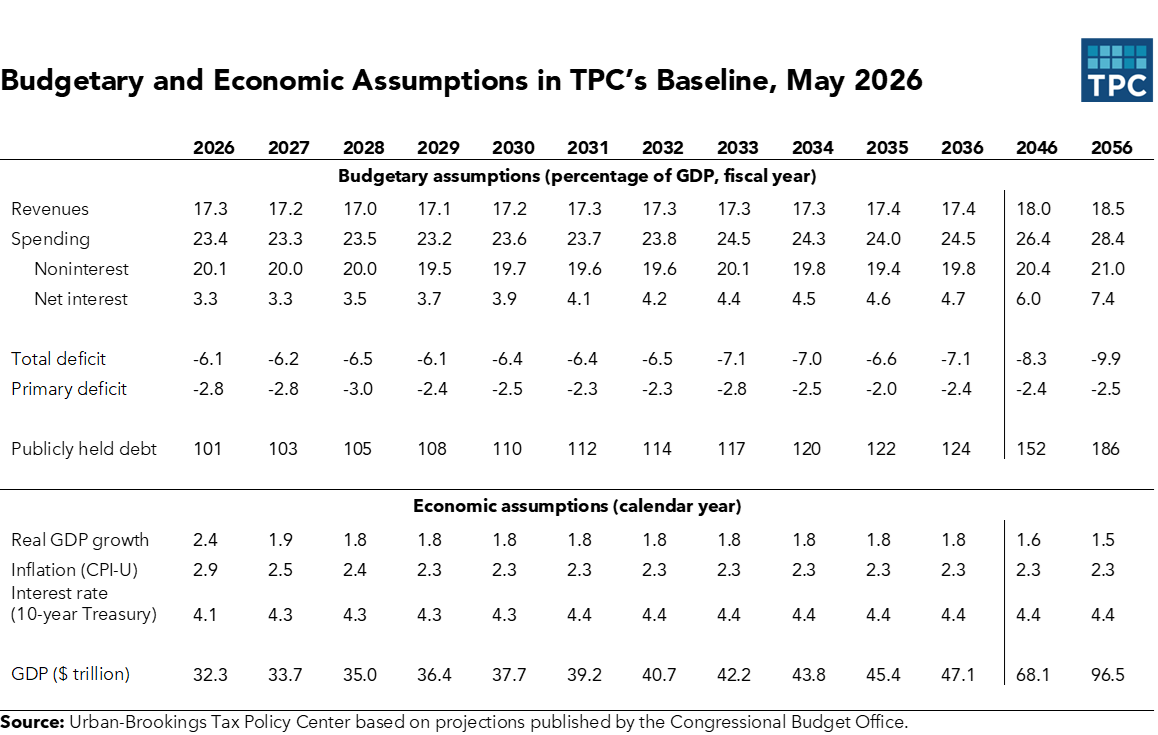

In constructing its baseline, TPC generally adopts projections from the Congressional Budget Office (CBO) because they are the standard benchmark used for legislation considered in the US Congress. CBO produces detailed projections of the economy, federal spending (including by budget account), revenues, demographics, and federal health subsidies. These projections are internally consistent and include information on key assumptions and sources of uncertainty.

TPC incorporates these baseline projections into its microsimulation model and related business and tariff models to estimate how current and proposed tax policies will affect federal revenues and the distribution of tax burdens. These models require detailed additional inputs about households, income sources, taxes, and other economic and demographic factors. TPC combines the latest available tax data with CBO’s economic and budget assumptions to project those variables forward. When significant legislation is enacted, we update our baseline to reflect official estimates from CBO and the staff of the Joint Committee on Taxation (JCT).

May 2026 Update

TPC’s current law baseline is generally consistent with CBO’s projections published in February 2026. That includes changes following the enactment of the 2025 reconciliation law, referred to as the One Big Beautiful Bill Act (OBBBA), on July 4, 2025. The OBBBA made permanent many expiring provisions of the 2017 Tax Cuts and Jobs Act (TCJA) and modified other tax laws beginning in 2025.

TPC adjusted federal revenues to reflect the February 2026 US Supreme Court decision invalidating tariffs imposed under the International Emergency Economic Powers Act (IEEPA). Because of uncertainty about timing and process, TPC has not incorporated budgetary effects of any tariff refunds resulting from the decision. TPC also has not adjusted CBO’s economic projections, consistent with how TPC, CBO, and JCT typically incorporate legislative changes that occur in between updates to its economic forecast.

Download the underlying data here.