Brief

Tax Debate 2017

February 27, 2017

This year, Congress will consider what may be the biggest tax bill in decades. This is one of a series of briefs the Tax Policy Center has prepared to help people follow the debate. Each focuses on a key tax policy issue that Congress and the Trump administration may address.

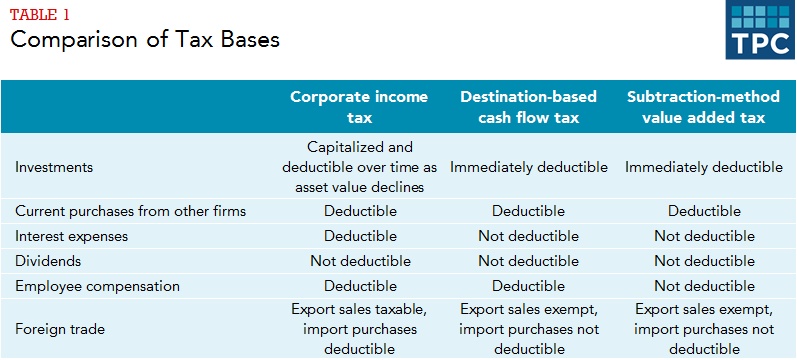

The destination-based cash flow tax (DBCFT) replaces the current corporate income tax (CIT) with a tax on corporate cash flow that is equivalent to a subtraction-method value added tax with a deduction for compensation of employees. The main differences between the DBCFT and the CIT are that 1) capital expenses are immediately deductible, instead of being deductible over the life of the asset, 2) interest expenses are not deductible, 3) export sales are tax-exempt, and 4) import purchases are not deductible. The DBCFT removes many of the problems of the current CIT by making the tax law more neutral among alternative investments, removing the tax preference for debt over equity in financing corporate investments, and removing incentives to invest and report profits overseas and for companies to abandon US residence through inversion transactions. However, the DBCFT creates new administrative problems, may be incompatible with international trade agreements, and would create significant windfall gains and losses and adjustment problems.

The CIT is imposed on corporate profits—the difference between sales revenues and deductible expenses. Deductible expenses include compensation of employees (cash wages and fringe benefits) and other expenses attributable to current sales, such as rent payments and interest paid to creditors. Firms cannot deduct the cost of capital assets immediately but instead deduct capital costs over time according to rules designed to align the timing of deductions with the revenues the assets generate. For example, firms can recover the costs of investments in machinery, equipment, and buildings over the productive lives of these assets through depreciation allowances. Firms deduct the costs of inventory when they sell goods held in inventory, with the deemed cost of any such sale determined by rules specifying whether the sale is from the most recent item purchased (last in-first out, or LIFO) or the earliest item purchased (first in-first out, or FIFO).

Capital expenses are not immediately deductible under the CIT because the purchase of a capital asset is not a cost to a company; it is simply an exchange of one form of wealth (cash) for another (a productive asset). The company incurs deductible costs only when the value of purchased assets declines, either through reduced productivity or a shorter future useful life (in the case of machines and buildings) or through disposal by sale (in the case of inventories). Depreciation and inventory accounting rules seek to properly measure the net income of businesses.

The CIT is a necessary complement to the individual income tax system because without it, profits that shareholders retain within corporations would escape tax. Corporate taxes in the United States and most other countries go further than simply taxing retained profits, however. Corporations cannot deduct dividends paid to shareholders, but shareholders must pay tax on those dividends under the individual income tax. Some countries have eliminated this so-called double taxation of dividends by allowing shareholders to claim a credit for corporate taxes attributable to their dividends or by applying a lower tax rate to dividend income received by individuals. Realized capital gains on corporate shares also face double taxation to the extent they reflect retained earnings of corporations (net of corporate tax) rather than improved expectations of future profitability.

Statutory US corporate tax rates range from 15 to 35 percent, with most profits facing the top rate. State corporate tax rates average a little over 6 percent, boosting the average combined state-federal rate to just over 39 percent after accounting for the deductibility of state taxes from the federal base. The effective tax rate (taxes divided by profits) is lower than the statutory rate because of special deductions, exemptions, and credits. The largest preference is accelerated depreciation, which allows companies to deduct capital costs, especially for machinery and equipment, at a faster rate than the assets decline in value. Companies also benefit from the immediate deductibility of research costs, a credit for research expenditures, a 9 percent deduction for domestic manufacturing profits, and numerous more narrowly targeted preferences. And multinational firms benefit to the extent they have foreign subsidiaries with earnings because the tax due on these earnings is deferred until the earnings are repatriated to the US-based parent firm. In addition, shareholders benefit from lower rates on dividends and long-term capital gains (a 23.8 percent top rate) than on ordinary income (a 43.4 percent top rate).

The DBCFT proposed by the House GOP to replace the CIT is a form of national sales tax that retains much of the structure (though not the substance) of the current corporate income tax. The House GOP DBCFT is different from the CIT in four major ways:

Expensing capital means that the DBCFT imposes no tax on the normal return from investment, in the sense that the pretax and after-tax rates of return are equal. By allowing expensing of investments, the government is essentially contributing 20 percent of a corporation’s costs. The government subsequently takes a 20 percent share of returns on the investments, which represents recovery of its share of the cost—the pretax rate of return is unchanged. However, profits that reflect the return on the value of assets in excess of their investment costs, such as patents and other sources of monopoly profits and economic rents, continue to be taxable. The House proposal would eliminate interest deductions to prevent firms from deducting interest costs on investments that generate tax-free income; otherwise firms could do this to reduce their tax liability without generating any additional net investment.

The CIT is different from the DBCFT and both are different from a subtraction-method value added tax (VAT), which is equivalent to a retail sales tax collected on the value added at each stage of production (table 1). The CIT taxes all receipts—from both domestic and foreign sales—net of all current costs (interest, employee compensation, and both domestic and imported purchases from other firms). Firms must capitalize investment expenses but can recover those costs over time. The CIT base thus equals the net income the corporation earns for its owners. (US-resident corporations pay CIT on their worldwide income but can defer tax on most profits earned abroad until they bring that income back to the United States.) In contrast, the VAT allows deduction of all purchases from other firms (including capital purchases), denies deductions for employee compensation and interest, exempts export sales, and taxes imports. The VAT base thus equals total sales by firms in the United States or, equivalently, consumption in the United States.

The DBCFT is much closer to a VAT than to the CIT. The only major difference between the DBCFT and the VAT is that the DBCFT allows deductibility of employee compensation. Adding a 20 percent flat rate tax on wages to the 20 percent DBCFT would make it exactly equivalent to a 20 percent VAT. The DBCFT is thus essentially a VAT with tax on the labor portion of value added collected from employees instead of firms. Imposing the tax on the labor contribution to value added on employees instead of on firms allows graduated rates on earnings instead of a single rate.

The DBCFT has three main advantages over the current CIT:

The DBCFT has significant drawbacks, however. Not taxing the normal return to capital at the firm level reduces tax progressivity because investment income is highly concentrated among upper-income taxpayers. Shifting to a destination-based tax raises taxes on importers substantially and gives firms that are large exporters permanent tax rebates from the Treasury. In theory, a uniform tax on imports and a rebate to exports should not affect either the trade balance or relative costs of importing and exporting firms because exchange rates should change to offset the effects of the taxes and rebates. So, for example, an importer will pay more tax but will also pay less for imported goods, leaving the net cost of imports unchanged. While neutralizing effects on trade flows, the exchange rate movement will generate capital gains and losses – US holders of foreign assets will see their purchasing power in the United States decline due to the rise in the dollar in terms of foreign currencies, while foreigner holders of US assets will receive a windfall benefit.

Firms and their political allies are unlikely, however, to buy the argument that exchange rates will offset the rebates and taxes. And the introduction of the tax will produce many losers, including highly leveraged domestic firms and foreign governments with large amounts of dollar-denominated debt. These wealth effects could cause significant economic dislocations, even if they are mitigated by transition rules that allow firms to continue to claim depreciation on existing assets and deduct interest on existing debt.

Firms would not all get equal rebates and taxes because individual owners of businesses taxed as pass-through firms, such as partnerships and S corporations, would pay a 25 percent tax rather than 20 percent. And the reluctance to allow profitable firms to pay negative corporate taxes will mean exporters will not likely be allowed to claim refundable credits from the Treasury, so many will not receive the full rebate. Firms could respond with increased use of leasing transactions and mergers and acquisitions designed to shift reported profits from firms with positive taxable income to firms with tax losses. If the border adjustments are not uniform and complete, as is likely, trade effects will give some firms special relief and make other firms and industries net losers. Finally, to the extent that certain sectors or industries are carved out from the DBCFT, efficiency gains from the tax shift will be eroded.