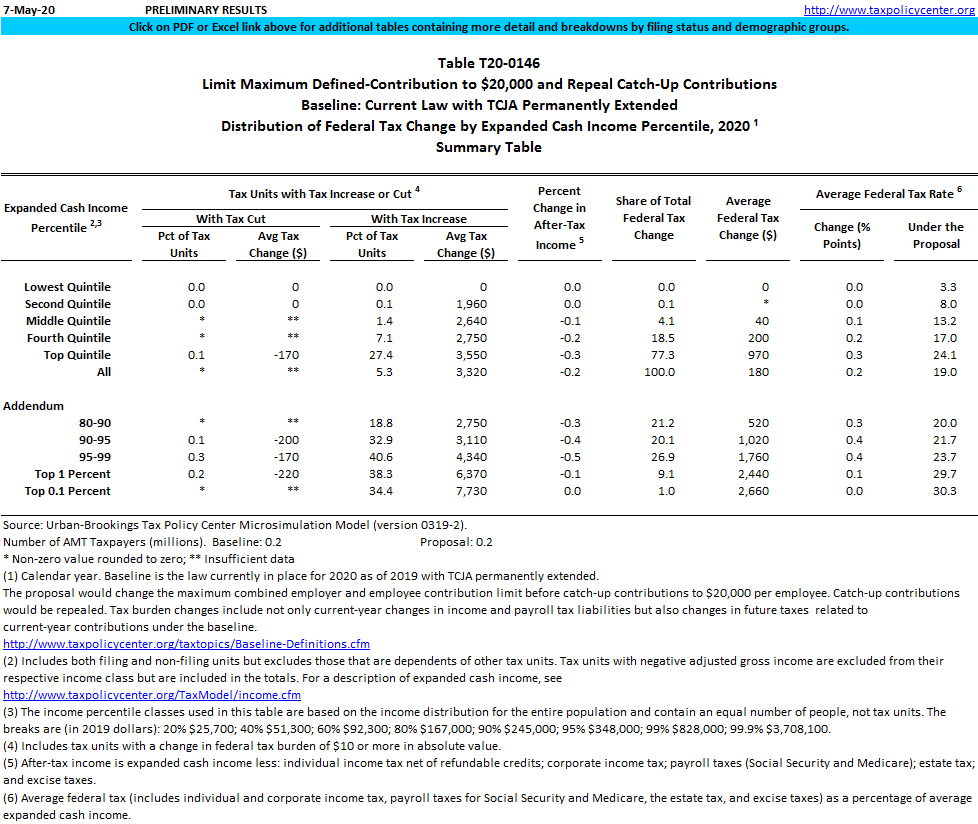

T20-0146 - Limit Maximum Defined-Contribution to $20,000 and Repeal Catch-Up Contributions, Baseline: Current Law with TCJA Permanently Extended, Distribution of Federal Tax Change by Expanded Cash Income Percentile, 2020

The proposal would change the maximum combined employer and employee contribution limit before catch-up contributions to $20,000 per employee. Catch-up contributions would be repealed. Tax liability changes include not only current-year changes in income and payroll tax liabilities but also changes in future taxes related to current-year contributions under the baseline. Baseline is the law in place as of December 18, 2019, with the Tax Cuts and Jobs Act of 2017 (TCJA) permanently extended.